Everything NVIDIA Depends On: The Hidden AI Supply Chain Behind the World's Most Important Stock

Everyone talks about NVIDIA. Almost nobody talks about what NVIDIA depends on.

NVIDIA is the face of the AI revolution.

Its GPUs power ChatGPT, Google Gemini, Microsoft Copilot, and virtually every major AI model being trained or deployed at scale today. Its stock has become a proxy for the entire AI trade.

But here is what most retail investors overlook:

NVIDIA does not build this alone.

Behind every H100, every Blackwell chip, every AI data center rack — is a massive, fragile, deeply interconnected global supply chain. And if any single part of that chain gets constrained, the entire AI buildout slows down.

That is exactly what this infographic maps out.

Let’s walk through every layer.

1. Chip Design Ecosystem: Where It All Begins

Before NVIDIA can manufacture anything, the chip has to be designed.

This is the least glamorous part of the supply chain — and one of the most important.

It includes companies like ARM, Synopsys, Cadence, and Ansys, which provide the chip architecture, IP blocks, electronic design automation (EDA) software, and simulation tools that allow NVIDIA’s engineers to design chips that push the limits of physics.

Without EDA software, there is no GPU blueprint. Without a blueprint, there is no chip.

This layer rarely gets attention. But it is the foundation of everything that follows.

2. Manufacturing & Equipment: The Real Chokepoint

This is arguably the most critical — and most fragile — layer in the entire NVIDIA ecosystem.

NVIDIA is a fabless company. It designs chips but does not manufacture them. For that, it depends on:

TSMC — the world’s most advanced chip foundry, manufacturing NVIDIA’s GPUs at the 4nm and 3nm nodes

Samsung Foundry — a secondary manufacturing partner

Intel Foundry — an emerging option as NVIDIA diversifies

But here is what most people miss:

TSMC depends on ASML.

ASML is the Dutch company that manufactures extreme ultraviolet (EUV) lithography machines — the only machines in the world capable of printing the most advanced chip designs. ASML holds a near-monopoly on this technology, and its next-generation High-NA EUV machines are now beginning to produce the chips that will power the next wave of AI infrastructure.

Applied Materials rounds out this layer, supplying the deposition, etching, and materials engineering systems that work alongside ASML’s machines to build the multiple layers inside a modern GPU.

The chain looks like this:

NVIDIA needs TSMC. TSMC needs ASML and Applied Materials. The AI boom depends on all of them scaling together.

This is the layer investors should watch most carefully for bottlenecks.

3. Memory Suppliers (HBM): The Bandwidth Problem

AI GPUs are not just about raw compute.

They are also about moving data — fast.

That is where High-Bandwidth Memory (HBM) comes in. HBM sits directly on the GPU and allows massive amounts of data to flow between the processor and memory at speeds that standard DRAM simply cannot match.

The three companies supplying HBM to NVIDIA are:

SK Hynix — currently the leading HBM supplier, with SK Hynix HBM3E powering NVIDIA’s H100 and H200 chips

Samsung — ramping HBM supply aggressively

Micron — a newer entrant gaining share in the HBM market

As AI models grow larger and data centers scale faster, HBM supply becomes one of the key constraints on how quickly NVIDIA can ship.

Memory is not a commodity here. It is a strategic chokepoint.

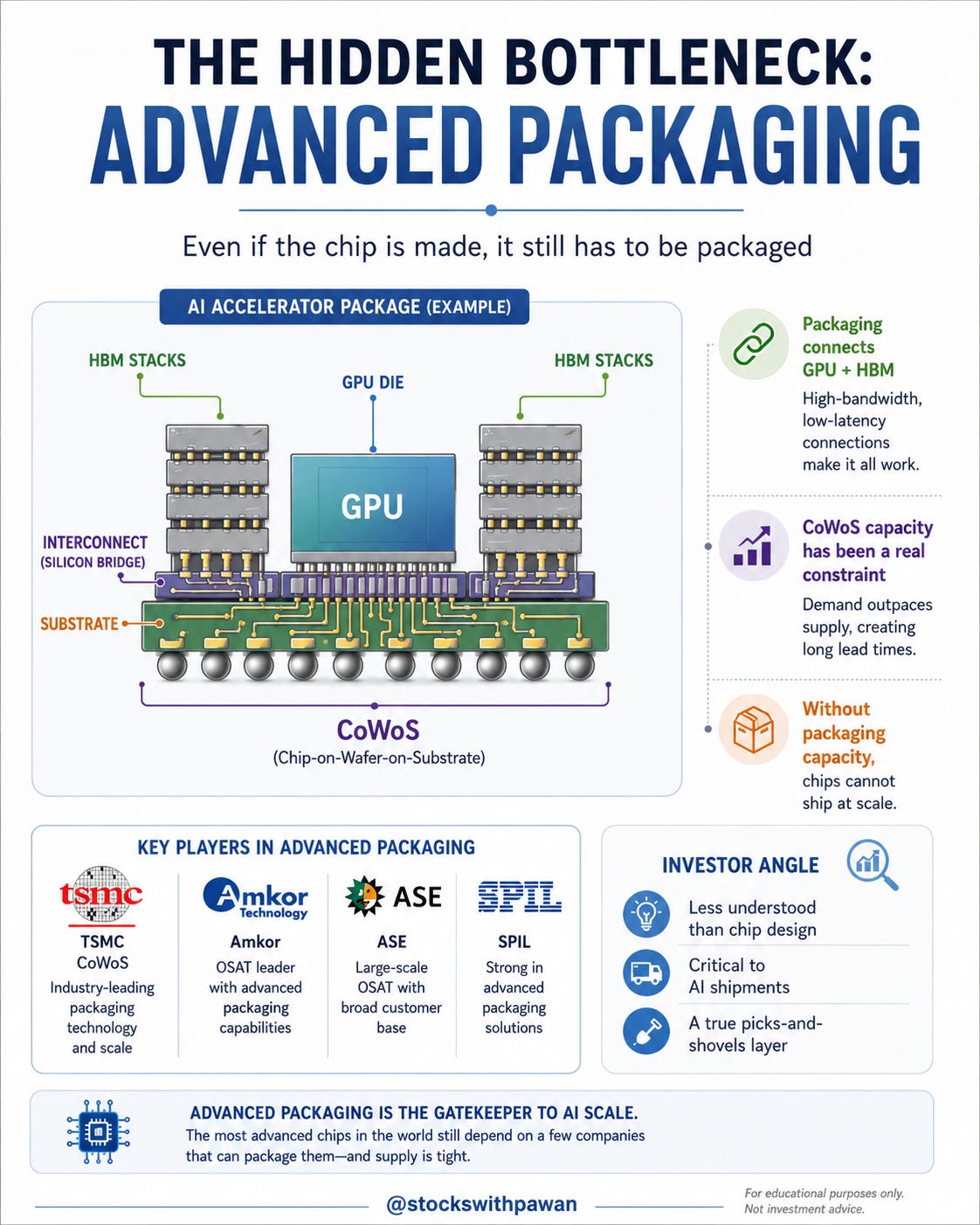

4. Advanced Packaging & Assembly: The Hidden Bottleneck

This is the layer most investors have never heard of — and it has been one of the biggest real-world constraints on NVIDIA’s ability to ship AI chips.

Modern AI accelerators are not single chips. They are complex systems that combine a GPU die, HBM memory stacks, and other components into a single package using advanced processes like CoWoS (Chip on Wafer on Substrate).

The companies that make this possible include:

TSMC CoWoS — NVIDIA’s primary advanced packaging partner

Amkor Technology — a leading independent packaging and testing provider

ASE Group — one of the world’s largest chip packaging companies

Siliconware Precision (SPIL) — another key assembly and testing partner

NVIDIA has locked in substantial CoWoS capacity with TSMC, reportedly reserving the majority of available capacity for 2024 and beyond. But packaging remains a genuine supply constraint that has limited GPU shipments in the past.

Even if demand is there, and even if wafers are ready — you still need packaging capacity to ship.

5. Systems & Server Partners: From Chips to Infrastructure

A GPU alone cannot power an AI data center.

NVIDIA chips need to be integrated into full server systems, rack-scale infrastructure, and deployable AI hardware that hyperscalers and enterprises can actually install.

This is where companies like Foxconn, Wistron, Inventec, and Quanta come in.

These are the contract manufacturers and ODMs (original design manufacturers) that build the physical servers and systems around NVIDIA’s chips. They are essential connectors between chip supply and real-world AI deployment.

NVIDIA has explicitly named Foxconn and Wistron as partners in its U.S. manufacturing expansion, with new supercomputer assembly facilities being built in Texas.

6. Cloud & Hyperscaler Demand: The Buyers Driving Everything

On the demand side, the engine pulling all of this forward is the hyperscaler and cloud ecosystem.

This includes Microsoft Azure, Google Cloud, Oracle Cloud, Meta, and Cloudflare — companies that are spending tens of billions of dollars annually on AI infrastructure and are the largest buyers of NVIDIA GPUs in the world.

AWS (Amazon Web Services), while not shown in the infographic, is another major buyer and worth noting.

This is why NVIDIA’s revenue visibility is so strong. It is not selling into a fragmented, unpredictable market. It is selling to a concentrated group of the largest and most well-capitalized technology companies in the world — all of whom are locked in a competitive race to build AI infrastructure.

7. High-Speed Connectivity & Optics: Moving Data at AI Scale

As AI clusters grow from hundreds to thousands to tens of thousands of GPUs, moving data between chips becomes just as important as computing with them.

This is where networking and optical connectivity come in.

Key players include:

Broadcom — custom AI networking chips and switching silicon

Marvell — custom AI accelerators and optical DSPs

NVIDIA Networking / Mellanox — InfiniBand and Ethernet networking for GPU clusters

Arista Networks — data center networking switches used in AI deployments

Corning — optical fiber and connectivity solutions

Corning recently announced a long-term partnership with NVIDIA to expand optical connectivity capacity specifically for AI infrastructure. The scale of modern AI clusters requires unprecedented volumes of high-performance fiber and photonics just to move data between GPUs.

The takeaway: AI data centers are not just chip farms. They are high-speed data movement machines. And the bigger they get, the more important the connectivity layer becomes.

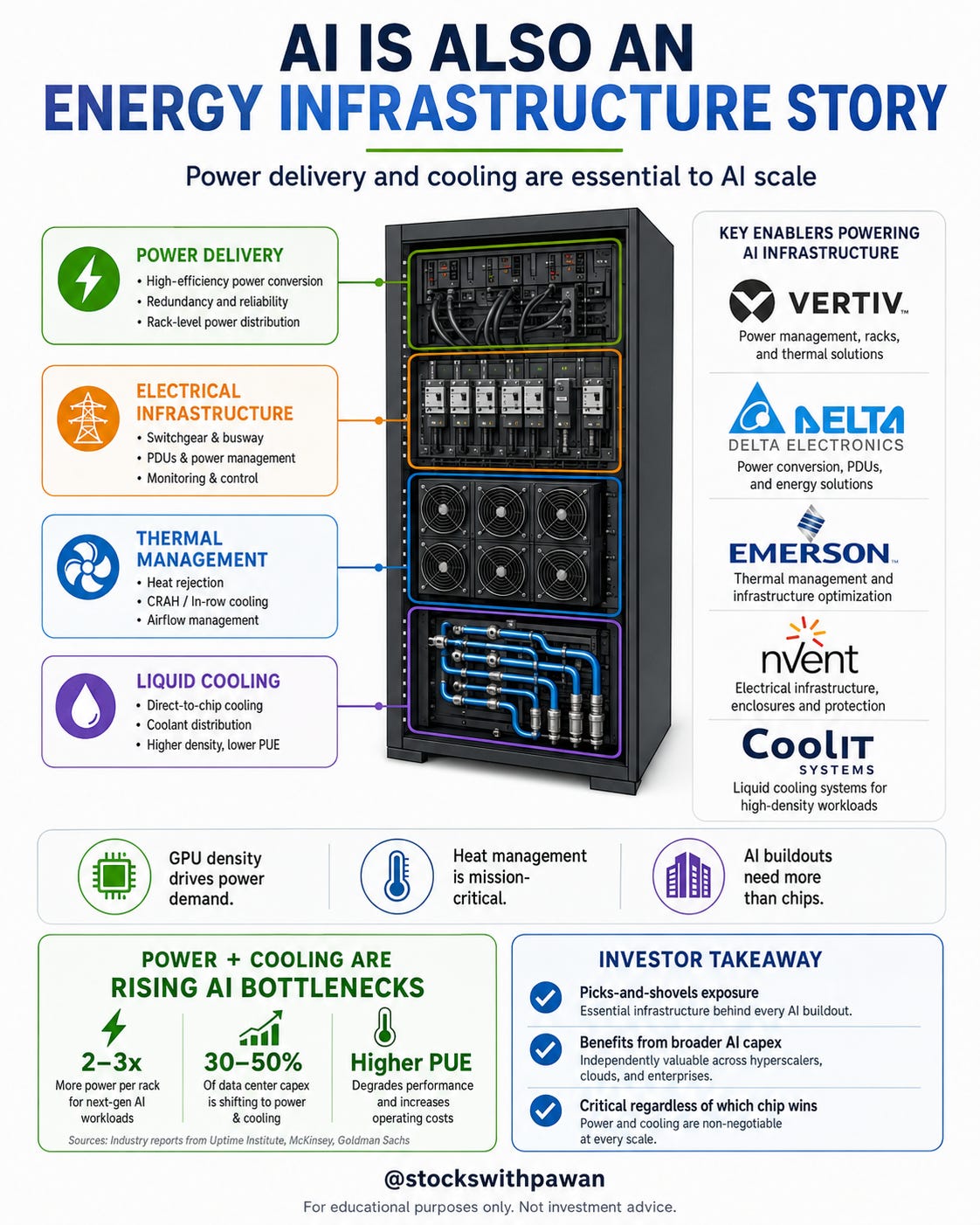

8. Power Delivery & Cooling: The Physical Reality of AI

Here is a number worth sitting with:

A single NVIDIA GB200 NVL72 rack — one of NVIDIA’s latest AI systems — can consume up to 120 kilowatts of power.

AI data centers are power-hungry, heat-generating machines. And that creates enormous demand for companies specializing in power delivery, cooling, and physical data center infrastructure.

This includes:

Vertiv — power and thermal management for data centers

Delta Electronics — power supplies and thermal solutions

Emerson — electrical infrastructure and data center power systems

nVent — enclosures and thermal management

CoolIT Systems — liquid cooling solutions for high-performance servers

This is one of the purest “picks and shovels” parts of the AI trade. Whether NVIDIA wins or a competitor emerges, AI data centers still need power and cooling. These companies benefit regardless of which GPU architecture dominates.

Raw Materials & Critical Inputs: The Base Layer Nobody Talks About

At the very bottom of the supply chain are the physical materials that everything else depends on.

Silicon wafers — Sumco and Siltronic

Copper — Freeport-McMoRan

Rare gases — Linde (used in chip manufacturing processes)

Rare earth elements — MP Materials (Mountain Pass mine, the primary U.S. rare earth operation)

Packaging substrates — Ibiden (a key supplier of the substrates used in advanced chip packaging)

AI may feel like it lives in the cloud. But the infrastructure behind it is deeply, unavoidably physical.

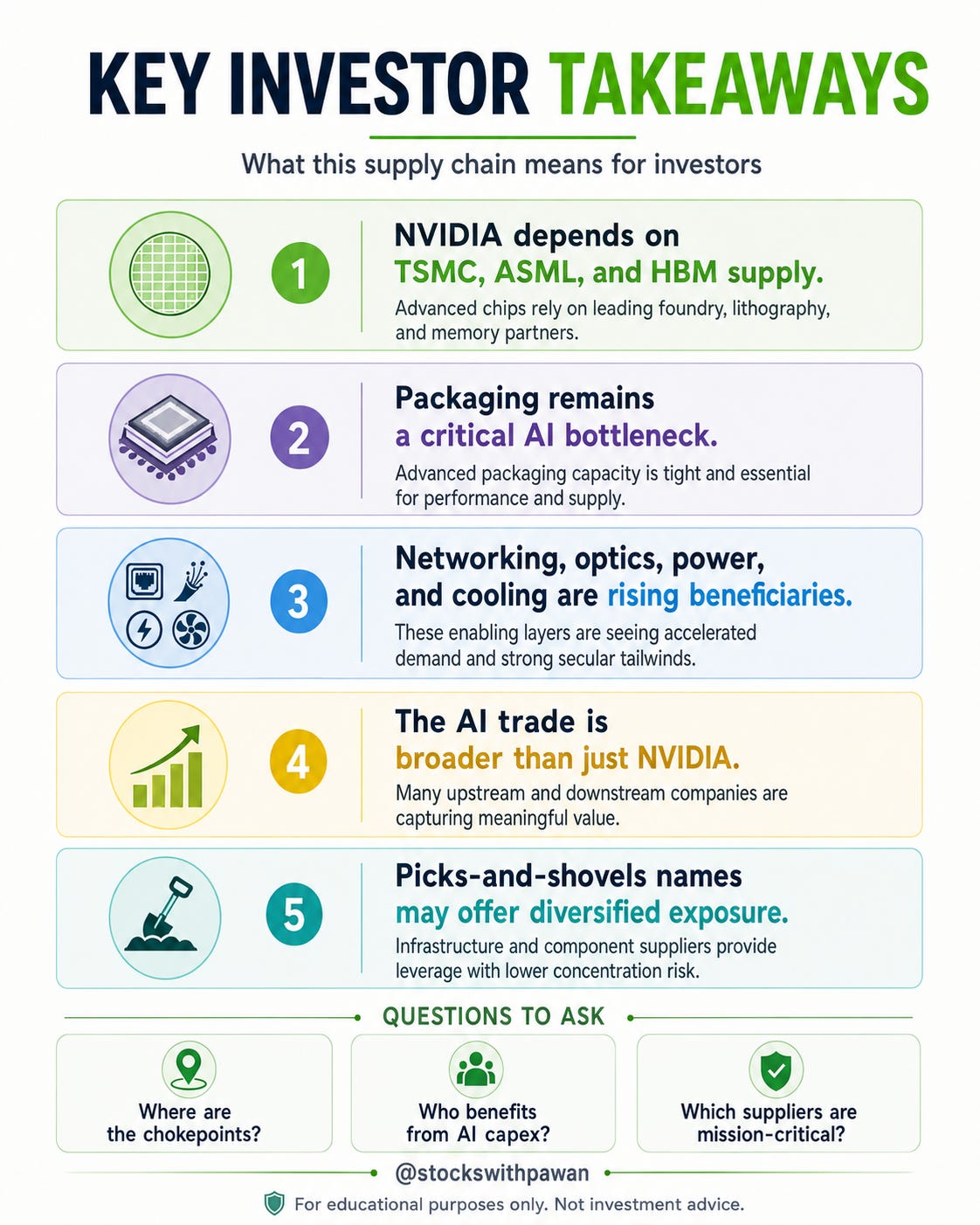

The Big Picture

NVIDIA is one of the most important companies in the world right now.

But NVIDIA’s growth is not a standalone story. It is the visible tip of a massive iceberg — a global supply chain that spans chip design software in California, lithography machines in the Netherlands, memory fabs in South Korea, packaging facilities in Taiwan, server assembly in Texas, and copper mines in Arizona.

Every layer matters. Every layer has potential bottlenecks. And every layer has companies that stand to benefit if AI infrastructure keeps scaling.

That is why the real AI research question is not just:

“Will NVIDIA keep growing?”

It is:

“Who supplies the tools? Who builds the factories? Who makes the memory? Who packages the chips? Who connects the servers? Who powers and cools the data centers?”

The market tends to price the obvious winner. The biggest opportunities often come from understanding what the winner depends on.

Not financial advice — just sharing what I’m researching and watching. Always do your own due diligence before making any investment decisions.

Follow along for more breakdowns of the AI supply chain and the companies building the infrastructure behind the boom.